Report: Subways and Buses Don’t Get Their Fair Share in MTA Capital Program

The current MTA capital plan disproportionately funds commuter rail at the expense of the subways and buses that account for 93 percent of the agency’s ridership — and those priorities should change, argues Nicole Gelinas in a new report for the Manhattan Institute [PDF].

With ridership falling and subway failures becoming too frequent and severe for politicians to ignore, the pressure to fix the transit system is intensifying. But the MTA has yet to demonstrate that it can select capital projects in the public’s best interest and execute them cost-effectively, Gelinas argues. The MTA isn’t investing in the right projects, and the projects it pursues consistently cost too much and run behind schedule.

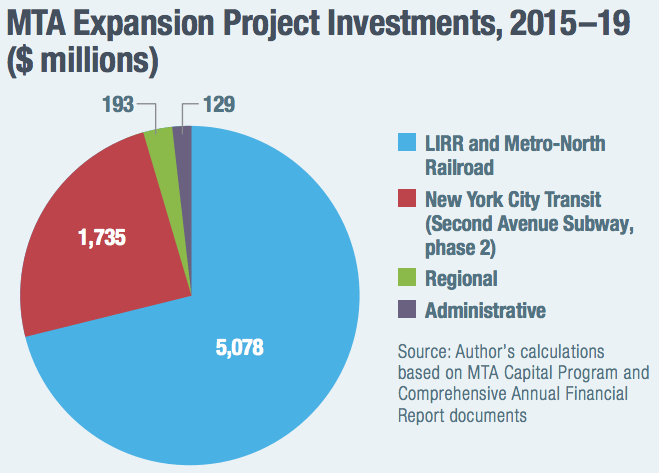

Looking at expansion projects, the 2015-2019 MTA capital plan spends $5.1 billion on the Long Island Railroad and Metro-North — nearly three times as much as the amount for subways and buses, even though the two commuter rail lines account for just 7 percent of MTA ridership.

The monster project is the East Side Access tunnel and terminal connecting LIRR to Grand Central, which is expected to cost more than $10 billion when it’s completed sometime next decade.

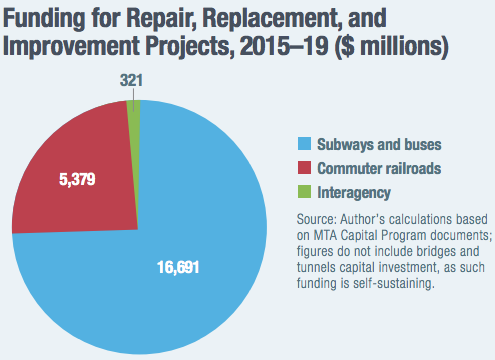

The capital budget for repairs and improvements to existing infrastructure is much less skewed toward commuter rail, but still doesn’t reflect the importance of subways and buses, with New York City Transit slated to receive 76 percent of the 2015-2019 funding pie.

“The MTA prioritizes commuter-rail projects that have value but improve service for fewer people, dollar for dollar, than a more assertive capital plan for subways and buses would,” Gelinas writes.

Getting the subway system to where it needs to won’t happen overnight. In the meantime, Gelinas says the MTA can ease the capacity crunch on the subways by investing in better bus service in cooperation with NYC DOT.

The MTA also needs to rein in its capital construction costs, which far outpace those of peer cities, and grapple with fixed costs like debt service and retiree pensions that are consuming a rising share of the agency’s resources.

“The MTA’s growing debt and retiree burden harms its flexibility to invest in physical infrastructure in the future,” she writes.

Read More:

Streetsblog has migrated to a new comment system. New commenters can register directly in the comments section of any article. Returning commenters: your previous comments and display name have been preserved, but you'll need to reclaim your account by clicking "Forgot your password?" on the sign-in form, entering your email, and following the verification link to set a new password — this is required because passwords could not be carried over during the migration. For questions, contact tips@streetsblog.org.